Top 10 Insane Insurance Coverages You Won’t Believe Exist in the USA

The American insurance industry is big and occasionally bizarre. Aside from the standard vehicle and health insurance, there are policies for some genuinely unexpected scenarios. This Blog looks at 10 insane insurance coverages available in the United States. From lost body parts “Whaaaat? They Insure That?!” to alien abduction (okay, maybe not aliens), prepare to learn some unusual yet curiously specific ways to protect yourself financially against the unexpected. So here are the top 10 most insane insurance coverages available in the USA.

1-Alien Abduction Insurance:

In the land of liberty and the pursuit of happiness, some Americans also pursue protection from…well, little green men. Enter Alien Abduction Insurance, a quirky insurance policy that injects a dose of humor into the world of risk management.

Not-So-Serious Safeguards: Unlike traditional insurance that shields you from everyday threats, alien abduction coverage focuses on the, shall we say, extraordinary. These policies typically don’t offer hefty payouts in case of an extraterrestrial encounter. Instead, they often come with tongue-in-cheek benefits like:

- Therapy sessions: To help you cope with the psychological effects of your alleged abduction (assuming they believe your story!).

- Sarcasm coverage: Because let’s face it, your friends and family might not be so quick to believe your tales of spaceships and probing. This “coverage” acknowledges the potential ridicule you might face.

- Double identity coverage: Maybe returning from an alien encounter leaves you needing a fresh start. Some policies jokingly offer coverage for establishing a new identity (because, you know, government cover-ups and all).

The Novelty Factor: Alien abduction insurance is more about novelty than actual financial security. The premiums are usually quite low, making it a lighthearted conversation starter or a funny gift for the UFO enthusiast in your life.

Where to Find It: Major insurance companies won’t be offering this type of coverage. Look for it from smaller, niche insurers who specialize in unusual policies.

So, is it worth it? Probably not for serious financial protection against alien visitors. But if you enjoy a good laugh or want a unique gift, then alien abduction insurance in the USA might be just the thing to add a touch of the extraordinary to the ordinary.

2-Zombie Apocalypse Insurance: Are You Prepared for the Undead?

In a world filled with uncertainties, one of the most unexpected scenarios might just be a zombie apocalypse. While it may seem like the plot of a Hollywood movie, some insurance companies in the USA are offering coverage for this unlikely eventuality. Zombie apocalypse insurance is a unique type of coverage that provides financial protection against the chaos and destruction that could result from a zombie outbreak.

What Does Zombie Apocalypse Insurance Cover?

Zombie apocalypse insurance policies vary from insurer to insurer, but they typically offer coverage for a range of scenarios that could arise during a zombie uprising. Here are some common features of these policies:

- Property Damage: In the event of a zombie invasion, your property could sustain damage from roaming hordes of the undead. Zombie apocalypse insurance can help cover the cost of repairing or replacing damaged structures, vehicles, and belongings.

- Loss of Income: If your business is disrupted or forced to close due to a zombie apocalypse, this coverage can provide compensation for lost income during the period of downtime.

- Evacuation Expenses: Should you need to flee your home or business to escape the zombie horde, insurance may cover evacuation expenses such as transportation, lodging, and emergency supplies.

- Defense Costs: In extreme situations, you may need to defend yourself or your property against zombies or looters. Some policies may cover the cost of weapons, ammunition, and fortifications.

- Medical Expenses: If you or your loved ones are injured during a zombie attack, insurance can help cover medical expenses, including hospitalization, surgery, and rehabilitation.

- Survivor Benefits: In the unfortunate event of death or zombification, some policies may provide survivor benefits to your designated beneficiaries or cover the cost of your funeral arrangements.

Is Zombie Apocalypse Insurance Worth It?

While the likelihood of a zombie apocalypse may be extremely low (or nonexistent), some individuals and businesses may find peace of mind in having this type of coverage. For hardcore survivalists or businesses with a sense of humor, zombie apocalypse insurance can be a fun and novel way to prepare for the unexpected.

However, it’s essential to approach these policies with a healthy dose of skepticism and to carefully review the terms and conditions. Like any insurance policy, it’s crucial to understand what is covered, what is excluded, and any limitations or restrictions that may apply.

Final Thoughts

Zombie apocalypse insurance may seem like a quirky gimmick, but it’s a testament to the creativity and adaptability of the insurance industry in addressing unique and unconventional risks. Whether you’re a die-hard zombie enthusiast or simply want to be prepared for any eventuality, there’s no denying the appeal of having coverage for the undead lurking around the corner. Just remember to keep your shotgun and canned goods handy – you never know when you might need them!

3-Lottery Winner Insurance: Protecting Your Big Prize

Winning the lottery is a dream come true for many, but what if your lucky day turns into a financial nightmare? That’s where lottery winner insurance comes in. In the USA, lottery winner insurance offers protection for businesses that offer large cash prizes through promotions or contests. Whether you’re running a sweepstakes, raffle, or other prize-based promotion, this coverage ensures that you can afford to fulfill your prize obligations, even if lightning strikes twice.

How Does Lottery Winner Insurance Work?

Lottery winner insurance works similarly to other types of prize indemnity insurance. Here’s how it typically works:

- Promotion Planning: Say you’re hosting a promotion with a grand prize of $1 million. While the odds of someone winning the jackpot are slim, you still need to budget for the possibility.

- Insurance Purchase: To protect yourself against the financial risk of a jackpot win, you can purchase lottery winner insurance from a specialized insurer. The cost of the insurance premium is based on factors such as the prize amount, the probability of winning, and the duration of the promotion.

- Prize Payout: If a participant wins the grand prize, the insurance policy kicks in to cover the cost of the payout. The insurer reimburses you for the prize amount, allowing you to fulfill your obligation without breaking the bank.

Why Do Businesses Need Lottery Winner Insurance?

Lottery winner insurance offers several benefits for businesses running promotions with large cash prizes:

- Risk Management: Hosting a promotion with a significant cash prize carries inherent financial risk. Lottery winner insurance mitigates this risk by providing a safety net in case someone actually wins the jackpot.

- Budgeting: By purchasing insurance, businesses can budget for the cost of the promotion more accurately. Rather than setting aside a large sum of money upfront, they can pay a predictable insurance premium based on the odds of a jackpot win.

- Promotion Enhancement: Offering a substantial cash prize can boost participation and excitement in your promotion. Lottery-winner insurance allows businesses to offer impressive prizes without putting their finances on the line.

- Peace of Mind: Running a promotion with a life-changing prize can be nerve-wracking. Lottery-winner insurance provides peace of mind, knowing that you’re protected against the unexpected.

Final Thoughts

Lottery winner insurance may not be as glamorous as winning the jackpot itself, but it’s a crucial risk management tool for businesses looking to offer large cash prizes. Whether you’re planning a sweepstakes, contest, or giveaway, this coverage ensures that you can celebrate your winners without worrying about the financial fallout. So go ahead, dream big, and let lottery winner insurance handle the rest.

4-Wedding Insurance in the USA: Protecting Your Big Day

Your wedding day is one of the most significant events of your life, but unexpected mishaps can turn it into a nightmare. That’s where wedding insurance comes in. In the USA, wedding insurance provides financial protection and peace of mind for couples planning their special day. From venue mishaps to unforeseen cancellations, this coverage ensures that you can say “I do” without worrying about the what-ifs.

What Does Wedding Insurance Cover?

Wedding insurance policies vary, but they typically cover a range of scenarios that could disrupt or derail your wedding plans. Here are some common features of wedding insurance in the USA:

- Vendor Cancellations or No-Shows: If a key vendor, such as your venue, caterer, photographer, or florist, fails to show up or goes out of business, wedding insurance can help cover the costs of rescheduling or finding a replacement.

- Extreme Weather: Unpredictable weather can put a damper on outdoor weddings. Wedding insurance can provide coverage if severe weather forces you to postpone or cancel your event.

- Illness or Injury: If you or your partner, a close family member, or a member of the bridal party falls ill or gets injured before the wedding, insurance can cover the costs of rescheduling or canceling the event.

- Venue Damage or Closure: If your venue is damaged or closes unexpectedly due to reasons beyond your control, such as fire, flooding, or bankruptcy, wedding insurance can help cover the costs of finding a new venue or rescheduling your event.

- Lost or Damaged Items: Wedding insurance can provide coverage for lost or damaged wedding attire, rings, gifts, or other personal property.

- Liability Coverage: Some wedding insurance policies include liability coverage, which can protect you against claims for property damage or bodily injury that occur during your wedding.

Is Wedding Insurance Worth It?

While no one wants to think about things going wrong on their wedding day, the reality is that accidents and unforeseen circumstances can happen. Wedding insurance offers peace of mind by providing financial protection against the unexpected.

Whether you’re planning an intimate backyard ceremony or a lavish ballroom affair, wedding insurance can help you protect your investment and ensure that your special day goes off without a hitch. With coverage options to suit every budget and wedding style, it’s a small price to pay for the peace of mind that comes with knowing you’re covered.

Final Thoughts

Your wedding day should be a joyous occasion filled with love and celebration, but it’s essential to be prepared for the unexpected. Wedding insurance offers a safety net against unforeseen mishaps that could threaten to derail your plans. Whether it’s a vendor no-show, extreme weather, or venue closure, this coverage ensures that you can focus on saying “I do” while leaving the what-ifs behind. So go ahead, dance the night away, and cherish every moment knowing that your special day is protected.

5-Fantasy Football Insurance: Protecting Your Fantasy Season

Fantasy football is a fun and competitive hobby, but leaving your team’s success entirely to chance can be stressful. Enter Fantasy Football Insurance, a relatively new concept designed to protect your investment and potentially salvage your season.

Here’s how Fantasy Football Insurance works:

- Coverage Options: Unlike traditional insurance with standardized plans, Fantasy Football Insurance offers flexibility. You can choose to insure your entire league entry fee, specific high-value players on your team, or even a combination of both.

- Triggering Events: Policies typically reimburse you for your league fee or insured player’s value if certain events occur during the season. These events can include:

- Season-ending injury: If a key player on your team suffers a season-ending injury, you can recoup some or all of the investment you made in drafting them.

- Suspension: A player’s suspension for violating league rules can derail your team’s performance. Fantasy Football Insurance might compensate you for the lost value.

- Unexpected retirement: The sudden retirement of a star player can throw your team strategy into disarray. Insurance can help offset the financial blow.

- Cost and Availability: Fantasy Football Insurance premiums are typically quite reasonable, costing a fraction of your league entry fee. However, this type of coverage isn’t yet as widely available as traditional insurance. You might need to search for specialized providers online or through fantasy football platforms that offer it as an add-on feature.

Is it Right for You?

Fantasy Football Insurance can be a valuable tool for:

- Competitive Players: If you take fantasy football very seriously and invest a significant amount of money in league fees and draft preparation, insurance can provide peace of mind and potentially save you from financial losses due to unforeseen circumstances.

- Risk-Averse Players: Even casual players can benefit from this coverage if they’d like some financial protection for their league entry fee.

Things to Consider:

- Read the Fine Print: As with any insurance policy, carefully review the terms, exclusions, and payout details before purchasing Fantasy Football Insurance.

- Not a Guarantee of Success: Remember, insurance protects against certain risks, but it doesn’t guarantee your fantasy team will win. Building a strong team through strategic drafting and managing your roster throughout the season remains crucial.

Overall, Fantasy Football Insurance is an innovative concept that can add a layer of security to your fantasy football experience. By understanding how it works and if it aligns with your playing style and risk tolerance, you can decide if it’s the right strategy to protect your fantasy football season.

6-Haunted House Insurance: Protecting Against the Paranormal

Haunted houses are all about scaring the bejeezus out of people, but for the operators, there’s a very real need to manage risks and protect their business. That’s where Haunted House Insurance, a niche insurance product specifically designed for these spooky attractions, comes in. It’s not about warding off actual ghosts, but rather safeguarding against the more earthly bumps and bruises that can occur during the haunt season.

Why Haunted House Insurance?

Running a haunted house is no small feat. It involves logistics, staff, elaborate sets, and of course, startled guests. Here’s where Haunted House Insurance provides a safety net:

- General Liability: This is the cornerstone of any haunted house policy. It protects your business in case a guest gets injured due to a slip and fall, bumps into a prop, or has a heart attack from a good scare (hopefully not too good!). Coverage extends to medical expenses and potential lawsuits.

- Medical Payments: Even minor injuries can happen. This coverage helps offset medical costs if a guest requires basic first aid on-site.

- Property Damage: Haunted houses can involve pyrotechnics, special effects, and intricate sets. If a guest accidentally damages a prop or your equipment malfunctions and damages the venue, this insurance can help cover repairs or replacements.

Haunt-Specific Coverage:

Beyond the general stuff, Haunted House Insurance often includes unique coverages tailored to the industry:

- Cancellation Coverage: Imagine having to shut down your haunt due to unforeseen circumstances like bad weather or a power outage. This coverage can reimburse you for lost revenue and non-refundable deposits.

- Props and Costumes: Elaborate costumes and sets are a haunted house’s lifeblood. This insurance can cover them in case of theft, vandalism, or damage during operation.

- Fright Actor Injuries: Accidents can happen even to your scare crew. This coverage can help with medical expenses if a staff member gets hurt while performing.

Cost and Availability:

Haunted House Insurance costs vary depending on the size and complexity of your haunt, its duration, and your claims history. Generally, it’s a few hundred to a few thousand dollars per season. Finding coverage can involve contacting specialized insurance brokers or companies that cater to the entertainment industry.

Peace of Mind for a Spooky Season:

Haunted House Insurance may not protect against bumps in the night, but it does offer peace of mind for haunt operators. By managing potential risks financially, you can focus on delivering a terrifying and safe experience for your guests, ensuring a successful and scream-filled season.

7-Body Part Insurance in the USA: Protecting Your Most Valuable Assets

Body part insurance in the USA isn’t a common policy you’ll find advertised everywhere. It’s a niche market targeting a specific group: people whose careers hinge on the exceptional function of certain body parts.

Here’s a breakdown of this unique insurance concept:

Who Needs It?

Imagine your livelihood depending on the dexterity of your hands as a surgeon, the flawless pitch of your voice as a singer, or the powerful kicks of a professional soccer player. These individuals have a vested interest in protecting their most valuable assets – their bodies. That’s where body part insurance comes in.

How Does It Work?

Unlike traditional insurance with set premiums and payouts, body part insurance is highly customized. Here’s the gist:

- Valuation: The first step involves a detailed evaluation of the body part in question. This considers factors like the insured’s profession, income potential, and skill level. Based on this, a value is assigned to the body part.

- Coverage Options: Policies can cover a single body part (e.g., a musician’s hand) or multiple parts (e.g., a dancer’s legs and ankles). The insurance kicks in if an illness or injury significantly impairs the function of the injured body part, leading to a loss of income.

- Payouts: The payout amount depends on the severity of the injury and the pre-determined value of the body part. It can be a lump sum payment or ongoing income replacement until the insured regains function or reaches retirement age.

Considerations and Limitations:

- Not for Everyone: Body part insurance is expensive and typically reserved for high-earning individuals in specific professions.

- Focus on Function, Not Aesthetics: While some might imagine insuring a model’s smile, this coverage is more about function than aesthetics. It protects income-generating abilities, not physical appearance.

- Maintaining Coverage: Maintaining a healthy lifestyle and adhering to safety precautions might be required to keep the policy valid.

A Safety Net for High-Value Careers:

Body part insurance offers a financial safety net for those whose careers depend on the peak performance of specific body parts. It’s a niche product, but for some professions, it can be a wise investment to protect their most valuable assets and ensure financial security in the event of a disabling injury.

8-Event Cancellation Insurance in the USA: Protecting Your Plans

In the unpredictable world of event planning, where unforeseen circumstances can wreak havoc on meticulous arrangements, Event Cancellation Insurance steps in as a financial savior in the USA. It acts as a safety net, protecting organizers from the significant costs associated with canceling or postponing an event due to covered reasons.

Why Event Cancellation Insurance?

Planning an event, whether a grand wedding, a corporate conference, or a music festival, involves substantial investments in venue rentals, vendor deposits, marketing materials, and more. Event cancellation insurance safeguards these investments by reimbursing you for non-refundable expenses if the event needs to be canceled or postponed due to:

- Adverse Weather: A sudden blizzard or hurricane can throw a wrench into your outdoor event plans. Insurance can help recoup costs associated with venue changes, marquee rentals, or even catering cancellations.

- Venue Issues: If your venue becomes unavailable due to unforeseen circumstances like a fire, power outage, or structural problems, the insurance can reimburse deposits and potentially cover relocation costs.

- Performer or Speaker Cancellation: A key speaker falling ill or a band member’s injury can disrupt your event. Insurance can help cover cancellation fees or replacement costs.

- Other Covered Reasons: Depending on the policy, additional covered reasons might include acts of terrorism, civil unrest, or unexpected illness of a key organizer.

Benefits and Considerations:

- Peace of Mind: Knowing you’re financially protected allows you to focus on planning a successful event without the constant worry of losing your investment.

- Customization: Event cancellation insurance policies can be tailored to the specific needs of your event, with varying coverage amounts and optional add-ons.

- Cost and Timing: The cost of the insurance is typically a small percentage of your overall event budget. However, it’s crucial to purchase the policy well in advance of the event, as coverage usually doesn’t apply to cancellations due to reasons known at the time of purchase.

Understanding the Fine Print:

Before purchasing event cancellation insurance, carefully review the policy details, including:

- Covered perils: Make sure the listed reasons for cancellation align with your potential risks.

- Exclusion clauses: Be aware of any situations not covered by the policy.

- Cancellation window: Understand the timeframe within which you can cancel the event to be eligible for reimbursement.

- Payout details: Know the process for filing a claim and the basis for calculating the reimbursement amount.

Event Cancellation Insurance: A Wise Investment

For anyone planning an event that involves significant financial commitments, Event Cancellation Insurance is a wise investment. It provides valuable peace of mind and protects your bottom line in case the unexpected disrupts your carefully laid plans. By choosing the right policy and understanding its coverage, you can ensure your event, and your investment is safeguarded against unforeseen circumstances.

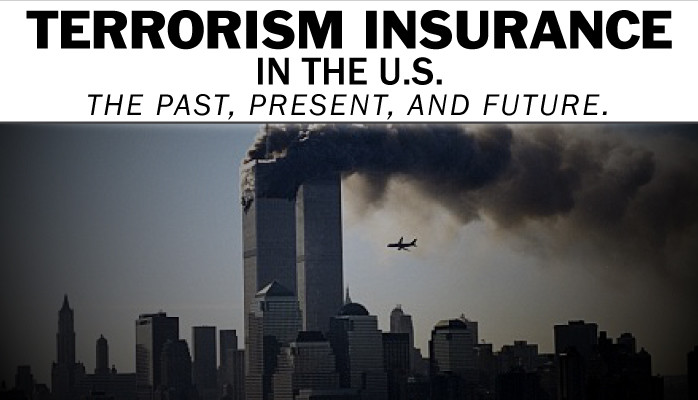

9-Terrorism Insurance in the USA: Protecting Businesses from the Unexpected

The threat of terrorism is a harsh reality, and businesses in the USA have a tool to manage the financial risks it poses: terrorism insurance. Let’s delve into what it is, how it works, and why it might be important for your business.

A Post-9/11 Response:

Following the devastating attacks of September 11th, 2001, private insurers became wary of covering terrorism risks due to the potential for immense losses. To address this gap, the US government established the Terrorism Risk Insurance Act (TRIA).

Public-Private Partnership:

TRIA creates a unique partnership between the public and private sectors:

- Private insurers are required to offer terrorism coverage to businesses as part of their property and casualty insurance policies.

- The federal government acts as a reinsurer, taking on a significant share of the financial burden if a large-scale terrorist attack occurs. This reduces the risk for private insurers, making terrorism coverage more affordable for businesses.

What Does It Cover?

Terrorism insurance policies typically provide coverage for three main areas:

- Physical damage: This covers damage to your property, including buildings, equipment, and inventory, caused by a certified act of terrorism.

- Business interruption: If a terrorist attack forces you to close your business or operate at a reduced capacity, the policy might reimburse you for lost income.

- Liability: Some policies might also cover your legal liability if someone is injured or killed on your property due to a terrorist act.

Obtaining Coverage:

While all property and casualty insurers must offer terrorism coverage, it’s not automatically included in your standard policy. You’ll need to specifically request it from your insurer and negotiate the terms of the coverage.

Cost Considerations:

- Premiums: The cost of terrorism insurance varies depending on several factors, including your location, business size and industry, and the level of coverage you choose. Generally, higher-risk areas and industries will have higher premiums.

- Deductibles: Terrorism insurance policies often have high deductibles, meaning you’ll be responsible for a significant portion of the initial loss before the insurance kicks in.

Is It Right for Your Business?

The decision to purchase terrorism insurance depends on your risk tolerance and the potential financial impact of a terrorist attack on your business. Here are some factors to consider:

- Location: Businesses in areas with a higher risk of terrorism or those considered critical infrastructure might be more likely to benefit from this coverage.

- Risk Tolerance: How comfortable are you absorbing the financial blow of a terrorist attack without insurance?

Conclusion:

Terrorism insurance provides valuable protection for businesses in the USA. By understanding how it works, the coverage it offers, and the factors to consider, you can make an informed decision about whether it’s the right choice for your financial security and peace of mind.

10-Pet Insurance in the USA: Ensuring the Well-being of Your Furry Friends

For many pet owners in the USA, their furry companions are cherished members of the family. From routine veterinary care to unexpected medical emergencies, the cost of keeping pets healthy can add up quickly. That’s where pet insurance comes in – offering financial protection and peace of mind for pet owners facing unexpected veterinary expenses.

What is Pet Insurance?

Pet insurance is a type of insurance policy that helps cover the cost of veterinary care for pets. Similar to health insurance for humans, pet insurance typically reimburses pet owners for a portion of eligible veterinary expenses, including:

- Illnesses: Coverage for treatment of illnesses such as infections, allergies, digestive issues, and more.

- Accidents: Coverage for injuries resulting from accidents such as broken bones, lacerations, and poisoning.

- Chronic Conditions: Coverage for ongoing or chronic conditions such as diabetes, arthritis, and cancer.

- Wellness Care: Some pet insurance policies offer optional coverage for routine wellness care, including vaccinations, annual exams, and preventive treatments.

How Does Pet Insurance Work?

Pet insurance works similarly to other types of insurance policies. Here’s how it typically works:

- Policy Purchase: Pet owners can purchase a pet insurance policy from a licensed insurance provider. Policies may vary in terms of coverage options, deductible amounts, reimbursement levels, and premium costs.

- Veterinary Visits: When a pet requires medical care, the pet owner pays the veterinarian directly for the services rendered.

- Claim Submission: After paying the veterinary bill, the pet owner submits a claim to the insurance company for reimbursement. This usually involves providing copies of the veterinary invoices and medical records.

- Reimbursement: Once the claim is processed and approved, the insurance company reimburses the pet owner for a portion of the eligible expenses, according to the terms of the policy. Reimbursement levels may vary depending on factors such as deductible amount and coverage limits.

Why Consider Pet Insurance?

Pet insurance offers several benefits for pet owners:

- Financial Protection: Pet insurance provides financial protection against the cost of unexpected veterinary expenses, ensuring that pet owners can afford necessary medical care for their pets without breaking the bank.

- Peace of Mind: Knowing that their pets are covered by insurance can give pet owners peace of mind, allowing them to make decisions about their pets’ health care based on what’s best for the animal, rather than what they can afford.

- Flexibility: Pet insurance policies offer flexibility in terms of coverage options, allowing pet owners to customize their coverage to suit their pets’ needs and their budget.

- Preventive Care: Some pet insurance policies offer coverage for routine wellness care, encouraging pet owners to stay proactive about their pets’ health by providing financial incentives for preventive treatments and exams.

While these insurance coverages may seem bizarre, they highlight the creativity and innovation of the insurance industry in addressing a wide range of risks and uncertainties. Whether you’re preparing for the zombie apocalypse or just looking out for your furry friend, there’s a policy out there for almost anything.

Until next time, take care and stay protected!